Why Financial Literacy is Important to College-Bound Teens

This is the second of two posts about U.S. teens’ results on a recent international assessment of financial literacy.

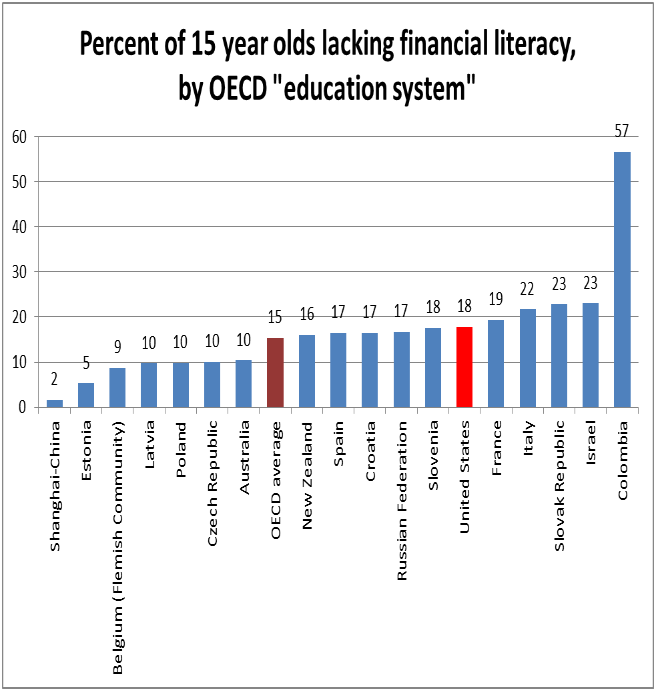

Every three years, the Organization for Economic Cooperation and Development (OECD) releases the results for the Program for International Student Assessment (PISA), an international assessment of math, science and reading literacy of 15-year-olds. In the latest PISA administration, all 34 OECD countries, plus another 31 partner countries, participated. For the first time, a financial literacy component was included in the 2012 assessment. Only a fraction of the countries that participated in the main PISA program chose to participate in the financial literacy exam.

Below, I chart the percentage of 15-year-olds that failed to hit the basic level of proficiency as defined by OECD. The financial literacy being tested is not about collateralized debt obligation, credit default swaps, hedge funds or any of the other super-complicated esoteric financial instruments that have made Wall Street rich. Rather it is about the basics of finance including balancing a checkbook, how to use a cash machine, identifying different costs in a supermarket, and understanding that risk can vary with different financial choices. For example, part of the tests assess 15-year-olds to see if they are confident and capable at handling and monitoring transactions and if they can

- use cash, cards and other payment methods to purchase items;

- use cash machines to withdraw cash or to get an account balance;

- calculate correct change;

- work out which of two consumer items of different sizes would give better value for their money, taking into account the individual’s specific needs and circumstances; and

- check transactions listed on a bank statement and note any irregularities.

In the United States, 18 percent of 15-year-old students scored below level 2 (the baseline of proficiency set by the OECD). While this is not statistically different than the OECD average, the stakes for Americans with low levels of financial literacy are probably higher than in many other countries on the list—in part because we are such a consumer-oriented economy with a smaller safety net than most of the other participating countries.

Specifically, consider that most of these 15-year-olds will soon be heading off to college and will need to figure out a way to finance their increasingly expensive postsecondary education. But with such low levels of financial literacy, we should not be surprised that so many of them are making loan decisions that will likely produce financial headaches for them and perhaps a giant migraine for the country. Student loan debt now tops out at over $1 trillion. And a large number of students are delinquent on their student loans. According to the Federal Reserve Bank of New York around 6.7 million borrowers (or 17%) are more than 90 days delinquent. Excluding the 44% of borrowers who are not yet in repayment, the delinquency rate rises to almost one-third.

As the PISA results demonstrate, too many young people are not equipped with the knowledge and resources to make wise financial decisions about college. The data from the growing problem of student loan defaults shows one of the main consequences of that illiteracy.

To help students avoid the traps of bad loan decisions, we need to improve overall financial literacy, but we also need to provide students with much better information about the likelihood that they will succeed in college and in the job market afterward. They need good information about the likelihood that they will graduate from college, how long it will take them to graduate, how much it will really cost and how much they are likely to earn after they graduate. This information has to be made available to students, their parents and their guidance counselors in an easy-to-use way, that can help students make wise college going decisions and wise borrowing decisions. The federal government’s College Scorecard helps a bit. But many states, such as Texas and Florida, are providing more detailed information and tools to help guide students into better decisions.

Mark Schneider is a vice president and Institute Fellow at AIR.