Medicare Enrollment Maze Puts Seniors at Risk for Penalties and Coverage Gaps

Wrong Turn in Switching from Private Health Insurance to Medicare Can Mean Coverage Gaps, Disrupted Care, Large Out-of-Pocket Costs and Lifelong Late-Enrollment Penalties

Washington, D.C.—An in-depth case study of 17 health insurance counselors, brokers, insurers, large employers and consumer advocates working with seniors suggests that as more Americans work past age 65, transitioning correctly from employer or other health coverage to Medicare is the No. 1 problem for seniors. This study was produced by the American Institutes for Research’s (AIR) Center on Aging.

Historically, most Americans’ eligibility for full Social Security retirement benefits and Medicare coverage dovetailed at age 65: Medicare enrollment was automatic when 65-year-olds signed up for Social Security retirement benefits. But since 2000, the age to collect full Social Security retirement benefits has gradually risen from 65 to 67, and people are working longer, slowly fraying the decades-old enrollment link between Social Security and Medicare and confusing millions of older Americans, according to the study.

“Seniors who take a wrong turn through the Medicare enrollment maze can face coverage gaps, disrupted care, large out-of-pocket costs, and lifelong late-enrollment penalties,” said Kathryn Paez, a principal researcher at AIR and lead author of the study.

“Seniors who take a wrong turn through the Medicare enrollment maze can face coverage gaps, disrupted care, large out-of-pocket costs, and lifelong late-enrollment penalties,” said Kathryn Paez, a principal researcher at AIR and lead author of the study.

When people turn 65, and they or a spouse keep working and maintain employer health coverage instead of retiring and enrolling in Social Security, they must proactively sign up for Medicare, especially Part B, which covers physician and other outpatient care. Otherwise, they risk coverage gaps and expensive lifelong Part B late-enrollment penalties. Other research has found that some 750,000 Medicare beneficiaries in 2014 were paying lifetime Part B late-enrollment penalties—on average, adding more than $8,000 to the lifetime cost of their Medicare Part-B premiums.

“Today, people who delay Social Security retirement benefits until after age 65 receive no official government notice about how to avoid penalties or gaps in coverage when they choose to enroll in Medicare later,” Paez said.

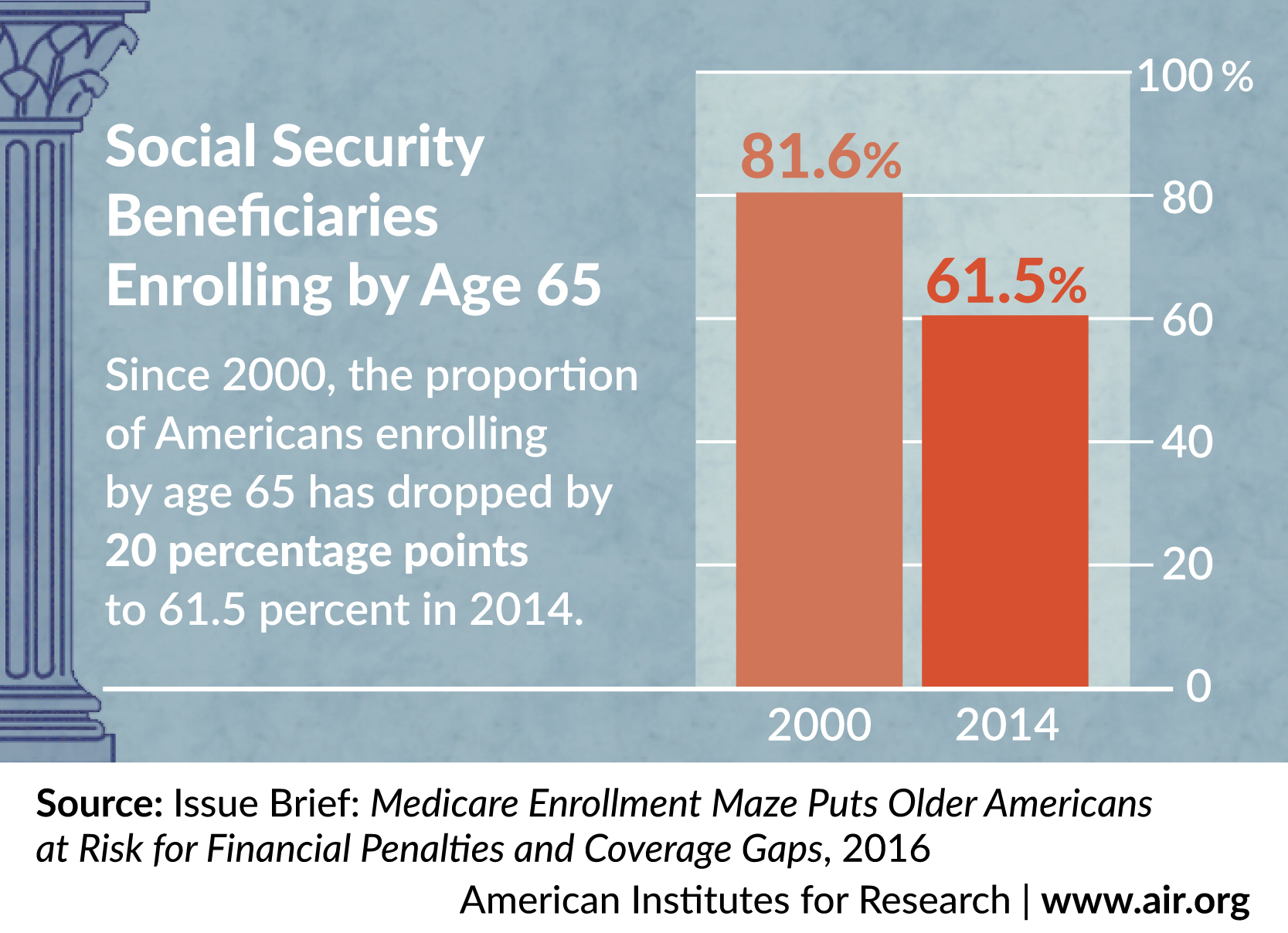

This problem is likely to worsen as the full Social Security retirement age reaches 67 for those born in 1960 or later and more Americans thus work past 65. Since 2000, the proportion of Americans enrolling by age 65 has dropped by 20 percentage points to 61.5 percent in 2014.

The study’s findings, based on interviews with State Health Insurance Assistance Program (SHIP) counselors, brokers and employers about the support they provide to Medicare beneficiaries and the problems beneficiaries encounter are detailed in two new AIR Center on Aging issue briefs—Medicare Enrollment Maze Puts Older Americans at Risk for Financial Penalties and Coverage Gaps and Medicare Complexity Taxes Counseling Resources Available to Beneficiaries.

Key findings include:

- Avoiding penalties when people continue to work past age 65 depends largely on whether their employer coverage is primary or secondary to Medicare. That, in turn, depends on whether coverage is based on current employment and the number of people employed by employer. In some cases, an individual must proactively enroll in Medicare during a special enrollment period or face lifelong Part B late-enrollment penalties and go up to 16 months without coverage.

- All Part B enrollment periods have different time frames for applying and schedules for when coverage takes effect. To confuse matters more, all Part B enrollment periods differ from the annual open enrollment period each fall when people can change their Medicare Part D, Medigap or Medicare Advantage coverage.

- People who miss the Part B enrollment window also face paying a lifetime late-enrollment penalty equal to 10 percent of the standard Part B premium for each full 12-month period they could have had Part B had they enrolled. Over a lifetime, the penalties can add up. For example, typical women paying a 30-percent late fee will pay $9,769 extra for Part B coverage; men, whose life expectancy is shorter, can expect to pay $8,641.

- Even with an extensive portfolio of online and print resources, many beneficiaries need personalized counseling to understand their options and make informed choices. The SHIPs—state-run programs that receive federal grants—train and manage a network of staff and volunteer Medicare counselors who provide free counseling to beneficiaries.

- Medicare beneficiaries are inundated with mail and ads about Medicare plans when they turn 65 and during the annual fall open enrollment period. Feeling overwhelmed and unsure of where to start, some beneficiaries seek out a SHIP or broker. Others may want a second opinion after doing their own research.

- SHIP appears to be a highly cost effective way to provide one-on-one support to help Medicare beneficiaries make more informed choices about their coverage. In 2013, the $52 million spent on SHIP provided one-on-one counseling to more than 2.6 million of the 52.5 million Medicare beneficiaries at a cost of less than $20 per beneficiary served.

- Possible policy solutions include requiring the federal government to notify all people approaching age 65 of Medicare enrollment requirements, educating employers about transitioning older workers to Medicare coverage, streamlining and harmonizing Medicare enrollment periods, enhancing health insurance counseling services for older Americans, and strengthening appeal rights for beneficiaries facing late-enrollment penalties.

About AIR

Established in 1946, with headquarters in Washington, D.C., the American Institutes for Research (AIR) is a nonpartisan, not-for-profit organization that conducts behavioral and social science research and delivers technical assistance both domestically and internationally in the areas of health, education, and workforce productivity. For more information, visit www.air.org.

###